🗓️ December 2021 Updates

Keeping HR leaders up to date with important compliance updates and human resource articles.

Courts Halt Federal Vaccination Mandates Amid Legal Challenges

The Biden Administration’s various vaccine and/or testing mandates for employers with over 100 employees, certain healthcare providers and federal contractors, continue to face significant legal challenges. The following is an update on the status of these challenges:

OSHA ETS: The federal Sixth Circuit Court of Appeals based in Cincinnati has been selected to preside over the litigation concerning OSHA’s Emergency Standard (ETS) requiring companies with at least 100 employees to mandate COVID-19 vaccinations or submit to weekly testing and mask requirements. The ETS imposed two compliance deadlines – proof of vaccination and mask-wearing for unvaccinated employees beginning December 6, and the additional requirement of weekly testing for unvaccinated employees beginning January 4. Prior to the case being transferred to the Sixth Circuit, the Fifth Circuit Court of Appeals issued a nationwide stay of the ETS, which currently remains in effect.

OSHA has requested the Sixth Circuit to dissolve or modify the stay. The Sixth Circuit has released a timeline for parties to file briefs, responses and replies with a final filing date of December 10. This means that the Sixth Circuit is unlikely to take further action until approximately mid-December. In the meantime, OSHA has made it clear that it will stand down on its efforts to implement the ETS pending further litigation.

The Sixth Circuit’s decision may not be an “all or nothing” outcome. In its Emergency Motion to dissolve the stay, OSHA requested that the Sixth Circuit modify the stay to allow certain components of the ETS go into effect if the stay is not lifted in its entirety. Specifically, OSHA requested that the masking and testing requirement remain in effect pending the litigation of the stay and that the stay may be limited to allow employers the option to adopt COVID-19 policies, notwithstanding any state or local laws that may restrict such policies.

For now, employers who would otherwise be covered by the ETS should still remain prepared to comply in the event the stay is issued. However, the ETS is currently stayed until December 10 and, unless the stay is lifted, either as a result of OSHA’s request to dissolve or at a later decision of the Court, the ETS will not take effect.

Healthcare Employers – CMS Final Rule: On Tuesday. November 30, a federal judge in Louisiana issued a preliminary injunction to block the start of the CMS Interim Final Rule. The injunction applies nationwide except for ten states that are already under a preliminary injunction order issued on November 29 in Missouri.

The CMS Rule was released on November 5, and established conditions of participation on various Medicare and Medicaid certified providers and suppliers. Generally, the rule mandated that covered staff must be fully vaccinated by January 4. The CMS Rule also set a deadline for accommodation requests and receipt of the first vaccine dose by December 6. As of now, these conditions are halted nationwide. Healthcare employers should continue to monitor state and local laws that will impact existing employer vaccine mandates. In the meantime, covered employers who do not wish to proceed with a vaccine mandate may pause their efforts to comply with the CMS Rule. However, these preliminary injunctions are likely to be appealed, and thus healthcare employers should be ready to proceed with the requirements of the rule should the controlling injunction be reversed.

Federal Contractors and Subcontractors Vaccine Mandate: Separately, on Tuesday, November 30, a federal judge in Kentucky issued a preliminary injunction blocking the implementation of the vaccine mandate for federal government contractors and subcontractors. The ruling is limited to the three states, Kentucky, Ohio, and Tennessee that challenged the Federal Contractor and Subcontractor mandate. It is the first ruling against the contractor mandate but may be an indicator of additional challenges in light of the success of this first challenge.

IRS Proposes Extension of ACA Reporting Deadlines & Final Forms for 2021

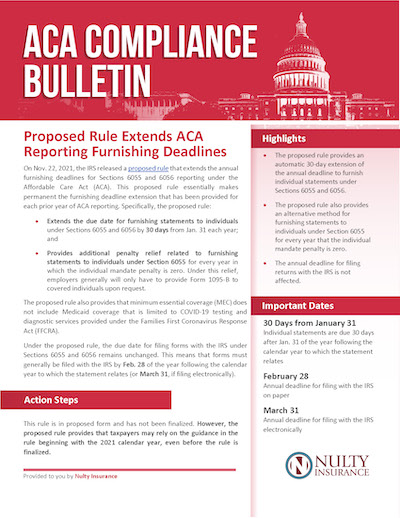

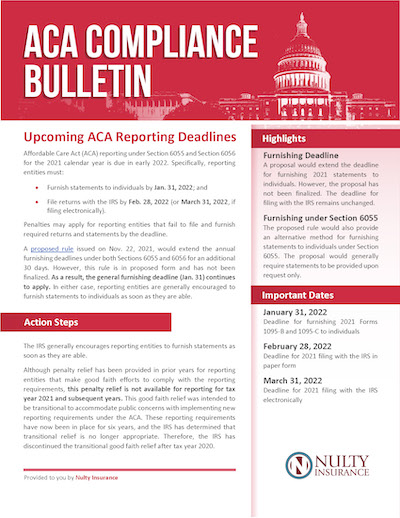

On November 22, 2021, the IRS issued proposed regulations that, if finalized (which will likely happen), will permanently extend the deadline to furnish Forms 1095-C and 1095-B to individuals, and in limited circumstances, provide an alternative method of furnishing these forms to individuals. In addition, the IRS reiterated its position that 2020 will be the last year of good-faith reporting relief with respect to ACA reporting. The proposed regulations also provide that Medicaid coverage limited to COVID-19 testing and diagnostic services is not “minimum essential coverage” under the ACA.

The proposed deadline to furnish Forms 1095-B & 1095-C to individuals provides an automatic 30-day extension, which generally means that the January 31 deadline will be extended to March 2. The proposed regs do not extend the deadline to file these forms with the IRS. Reporting entities generally must file these forms with the IRS by February 28 (if filed on paper) or March 31 (if filed electronically).

The proposed regulations provide alternative methods of furnishing Forms F1095-B & 1095-C to individuals, providing that in limited circumstances, the IRS will continue to not penalize entities for the failure to furnish information to individuals using Form 1095-B and in some cases, Form 1095-C. For insurers and “non-large” employers that sponsor self-funded group health plans, the entity must still prepare and file Form 1095-B with the IRS. However, these entities are not required to furnish individuals with a copy of Form 1095-B as long as the entity satisfies the several requirements.

The IRS may impose penalties of up to $280 per form for failing to furnish an accurate Form 1095-B or 1095-C to an individual and $280 per form for failing to file an accurate 1095-B & 1095-C with the IRS. The IRS indicated that it would not impose these penalties for incomplete or inaccurate forms for the 2020 calendar year (due in 2021) if the reporting entity can show that it “made good faith efforts to comply with the information reporting requirements.” This good-faith reporting relief does not apply to forms that were not timely furnished to individuals or filed with the IRS. In the proposed regulations, the IRS reiterated its position that the extension for 2020 will be the final extension of the good-faith reporting relief, but entities may still be able to avoid penalties if the entities can show that they had reasonable cause for the failures.

The IRS released the final 2021 forms for reporting under Internal Revenue Code Sections 6055 & 6056:

• 2021 Forms 1094-B and 1095-B are the forms that will be used by providers of minimum essential coverage (MEC), including self-insured plan sponsors that are not applicable to large employers (ALEs), to report under Section 6055.

• 2021 Forms 1094-C and 1095-C are the forms that will be used by ALEs to report under Section 6056 and for combined Section 6055 and 6056 reporting by ALEs who sponsor self-funded plans.

No substantive changes were made to the forms for 2021. Final instructions have not been released yet. However, draft instructions for Forms 1094-B and 1095-B as well as for Forms 1094-C and 1095-C are available which include updated penalty maximums for 2021.

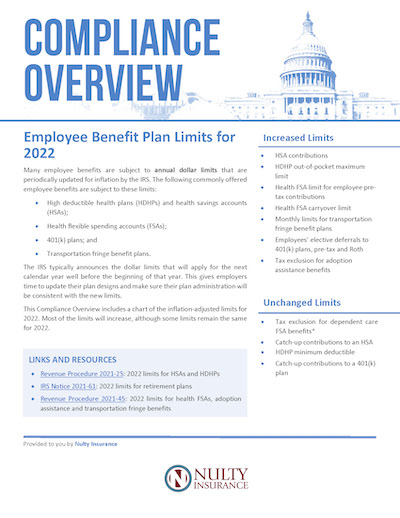

Employee Benefit Plan Limits for 2022

In mid-November, the IRS announced the 2022 contribution limits for flexible spending accounts (FSA), commuter benefits, and more.

Here’s a look at what’s changing:

• Health FSA: $2,850 (increased from $2,750). This also applies to limited purpose FSAs.

• FSA Carryover: $570 (increased from $550). Important note – under the CAA, employers can allow participants to rollover all unused FSA and dependent care funds to plan years ending in 2022 but not beyond.

• Commuter (Parking & Transit): $280 per month (increased from $270).

• Dependent Care: The annual limits will revert to $5,000 for single taxpayers and married couples filing jointly, or $2,500 for married people filing separately.

• Qualified Small Employer HRA: $5,450 for individuals and $11,050 for family.

• HSA: $3,650 for individuals and $7,300 for family.

New Rule Requires Reporting on Medical & Prescription Drug Costs

On November 17, 2021, federal agencies released an interim final rule requiring health plans and issuers to report information regarding the cost of prescription drugs and certain medical expenses. This rule is a continuation of the Biden administration’s efforts to promote greater transparency in health care spending.

As a reminder, this rule requires plans and issuers in the group and individual markets to submit certain information on prescription drug and other health care spending to federal agencies annually, including:

- General information about the plan and coverage

- Enrollment and premium information

- Total health care spending by enrollees versus employers and issuers

- Prescription drug rebates, fees and other compensation paid to the plan or issuer

- The 50 most frequently dispensed brand prescription drugs

- The 50 costliest prescription drugs by total annual spending

- The 50 prescription drugs with the greatest increase in expenditures from the previous year

- The impact of prescription drug rebates, fees, and other compensation on premiums and out-of-pocket costs

For 2020 and 2021 information, reporting must be submitted by December 27, 2022, and by June 1 of each year thereafter. Starting in 2023, federal agencies will issue biennial public reports on prescription drug pricing trends as well as the impact of prescription drug costs on premium out-of-pocket costs.

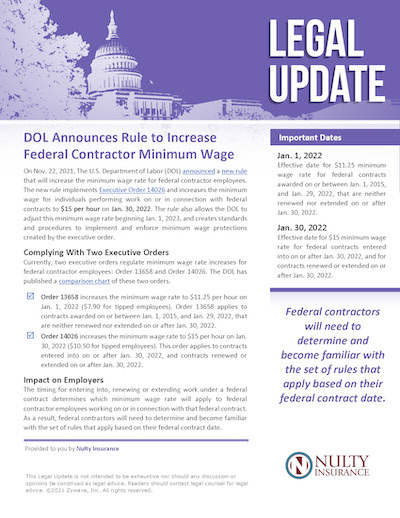

U.S. Department of Labor’s Wage & Hour Division Announces Final Rule to Increase Federal Contractor Minimum Wage

On November 22, 2021, the Biden administration published a final rule instituting a $15 minimum wage for certain covered federal contractors.

The new rule will apply to new or updated covered contractors beginning on January 30, 2022, and the required minimum wage will be updated annually for inflation.

In addition to new contracts and contract renewals, the minimum wage requirement will also apply when contracting agencies exercise options on existing contracts. Enforcement of the regulation will be the responsibility of the DOL’s Wage & Hour Division.

The IRS, DOL, and HHS issued interim final regulations to provide guidance regarding health care transparency provisions of the Consolidated Appropriations Act. This will apply to group health plans effective December 27, 2021. However, the Departments have announced a non-enforcement policy for the first year of applicability.

Live Well, Work Well Newsletter – December 2021

A free wellness resource to download and share in your workplace.

This month’s newsletter topics include:

-

Tips for Celebrating the Holidays Safely

- Reducing Your Holiday Stress

- Safety Tips While Decking the Halls

- Slow Cooker Beef Stew Recipe