🗓️ January Compliance Updates

Mandatory Coverage of COVID-19 Vaccines under Group Health Plans

December 11, 2020 – FDA issues an emergency authorization for the Pfizer COVID-19 vaccine and one day later, the Advisory Committee on Immunization Practices (ACIP) issued an interim recommendation for use of the vaccine in persons age 16 or older.

December 18, 2020 – FDA issues an emergency authorization for the Moderna COVID-19 vaccine and the following day, the ACIP issued another interim recommendation for use of the Moderna vaccine for persons age 18 or older. Alternative COVID-19 vaccines are likely to be approved by the FDA under emergency authority in the coming weeks. Group health plans are encouraged to prepare to cover the cost of the Pfizer, Moderna, and other approved COVID-19 vaccines.

Under the CARES Act, non-grandfathered individual and employer-sponsored group health plans are required to cover the entire cost of preventative services by not imposing cost-sharing in the form of deductibles, copays, or coinsurance. Thus, non-grandfathered individual and group health plans must cover the Pfizer vaccine as preventative care no later than Jan. 1, 2021, and the Moderna vaccine as preventative care no later than Jan. 8, 2021.

Your plan documents should reflect this coverage and participant communications should be distributed that provide information regarding the availability of COVID-19 vaccinations with no cost-sharing.

What Michigan Employers Should Know About the COVID-19 Vaccine

In early December, Michigan’s Director of Health and Human Services, Robert Gordon, said that the agency is not considering a statewide coronavirus vaccine mandate. Nonetheless, I am sure you are wondering whether and when you can require employees to take advantage of the vaccine. Well, there is currently no law or regulation directly addressing whether employers may mandate vaccination for COVID-19. Mandatory vaccination policies are controversial, especially outside the healthcare industry. Once the COVID-19 vaccine becomes widely available, employers should consider their options and policies carefully and take into consideration the following:

- If an employee objects to the vaccine for religious reasons, the employer will need to explore what reasonable accommodations it can provide without an undue hardship.

- If an employee declines a vaccination due to a medical condition or disability, the employer must engage in an interactive process with the employee to identify reasonable accommodations, if any.

- Consider whether the employer will cover any costs associated with administering the vaccination and how this will integrate with employer-provided health plans.

- Evaluate whether to provide additional paid leave to employees who receive the vaccine and become ill or need days off from work to recover.

- Review and update job descriptions to include essential functions that may be related to COVID-19 risks, such as customer or visitor interaction, travel requirements, and close contact with other employees.

- Develop a vaccination policy and procedure for requesting accommodation for religious or medical reasons.

Additionally, the EEOC has offered new guidance that answers some workplace vaccination questions. Employers may encourage or possibly require COVID-19 vaccinations, but policies must comply with the ADA, Title VII of the Civil Rights Act of 1964 and other workplace laws.

See Section K – EEOC Guidance on Vaccinations

Stimulus Bill Extends FFCRA Tax Credits but Not Leave Mandate

While the FFCRA may have expired on December 31, 2020, many of us have been carefully watching to see if Congress may extend it. The House and Senate reached an agreement on an emergency coronavirus relief and omnibus package which clarifies the following relative to the FFCRA:

- Mandated FFCRA leave ended on December 31, 2020

- As of January 1, 2021, covered private-sector employers may voluntarily provide paid leave that otherwise would have qualified for FFCRA if it had not expired, and if they do, they may take the tax credit associated with the leave.

- The tax credit may only be taken for leave through March 31, 2021

This means that private-sector employers with fewer than 500 employees may voluntarily continue to provide FFCRA benefits through March 31, 2021, and when they do, will remain eligible to take the tax credit for the leave. Also, as an important reminder, that under this legislation, employees are not entitled to additional FFCRA leave after December 31, 2020.

Amendments to Michigan Public Act 238 – update protections for workers who do not report to work when they or their close contacts have COVID-19:

In the last week of 2020, Governor Whitmer signed a bill that made some significant changes to Michigan Public Act 238, most especially the time period that the employer must restrict an employee from entering the workplace when they or their close contacts have COVID-19. This now aligns more closely with the CDC guidance.

Highlights of the Amendments

The definition of “close contact,” “isolation period,” and “quarantine period” are aligned with CDC guidelines.

The actual isolation and quarantine requirements have changes as follows:

- Isolation after a positive test: An employee who tests positive for COVID-19 must not work until ALL of the following conditions are met: 1) the CDC isolation period has passed, which is 10-days from the date of the positive test or 10 days from when the employee developed symptoms, whichever is later; 2) It has been at least 24-hours since the employee had a fever without medication; 3) all symptoms have improved.

- Isolation after primary symptoms but no test: An employee who has primary symptoms of COVID-19 must not work until EITHER of the following conditions are met; the employee receives a negative test, OR; the CDC isolation period has passed (currently 10 days after the onset of symptoms, it has been at least 24 hours since the employee had a fever without medication, ALL symptoms have improved).

- Quarantine after close contact with a person who tests positive for COVID: PA 238 now requires employees to quarantine only after close contact with a person who tests positive – it no longer requires quarantine after close contact with a person who only has primary symptoms of COVID-19 but has not tested positive. Also, it allows employees to return to work if EITHER of the following have been met: 1) 14-days have passed from the last date of close contact, OR; 2) the local health department or a health care provider has advised the employee that they can follow the CDC’s option to reduce the quarantine period to 10-days (without testing) or 7-days (with testing).

- Quarantine exemptions: PA 238 exempts several categories of employees (healthcare workers, first responders, child care employees, etc.) from the quarantine requirements. That exemption now applies ONLY if the employee’s in-person presence is strictly necessary to preserve the function of the facility and cessation of the facility would cause serious harm or danger to public health or safety. The list of employees who are exempt from the quarantine requirements now includes workers in the energy industry and others designated by the Director of the Michigan DHHS.

Consolidated Appropriations Act, 2021:

December 27, 2020 – President Trump signed the Consolidated Appropriations Act, 2021 into law. This $900 billion coronavirus relief package includes funding for unemployment benefits, direct economic payments to individuals, vaccine distribution and rental assistance.

The Act also included the following:

-

- The No Surprise Act: Protects consumers from surprise medical bills for emergency services provided by out-of-network providers and facilities, non-emergency services provided by out-of-network providers at in-network facilities, and air ambulance services. The Act applies to group health plans or health insurance issuers offering group or individual health insurance coverage and health care providers and facilities. Additionally, it applies to plan or policy years beginning on or after January 1, 2022.

- New Reliefs for FSA’s: Temporary rules have been put in place to provide relief for participants in health flexible spending arrangements (FSAs) and dependent care flexible spending arrangements (DCAPs) in light of the COVID-19 pandemic. These expand the opportunities for plan sponsors to amend their plans to give employees additional opportunities to use their currently unused FSA & DCAP balances through 2022, as follows:

- Carry Over of Unused Amounts: The Act provides that FSAs and DCAPs may permit participants to carry over any unused contributions remaining from the 2020 plan year to the plan year ending in 2021. May also permit participants to carry over any unused contributions remaining in the FSA or DCAP from the 2021 plan year to the plan year ending in 2022.

- Extended Grace Period: The grace period for using FSAs and DCAPs have extended the grace period for participants to use remaining balances for a plan year ending in 2020 or 2021, until 12-months after the end of the plan year. Additionally, FSAs may permit participants who cease to participate during calendar 2020 or 2021 to continue to use the remaining contributions for reimbursements through the end of the plan year.

- DCAP Carry Forward: The current DCAP rules limit reimbursement of qualifying dependent care expenses to children under age 13. The Act provides that DCAPs may extend the maximum age for dependents from 12 to 13 for eligible dependents who turned 13 during the last plan year with an open enrollment period ending on or before January 13, 2020. Participants are therefore permitted to use unused balances for qualifying reimbursements for expenses incurred on behalf of dependents who aged out during the pandemic. Employers can allow unused dependent care FSA amounts for children until they turn age 14, at least through the end of the 2021 plan year.

- Midyear Election Changes: In recognition of the continued impact that COVID-19 has had on the ability of participants to maximize the use of their HSA and DCAP benefits, the Act affords participants the opportunity to change existing FSA and DCAP elections for 2021 midyear election changes in the absence of a change in status is consistent with IRS, which permitted such midyear elections during 2020.

- Amendment Deadline: Employers may amend their FSAs and DCAPs to take advantage of the flexibility offered by the Act, no later than the last day of the first calendar year beginning after the end of the plan year in which the change took effect. Accordingly, if the change takes effect January 1, 2021, the plan will need to be amended no later than December 31, 2022.

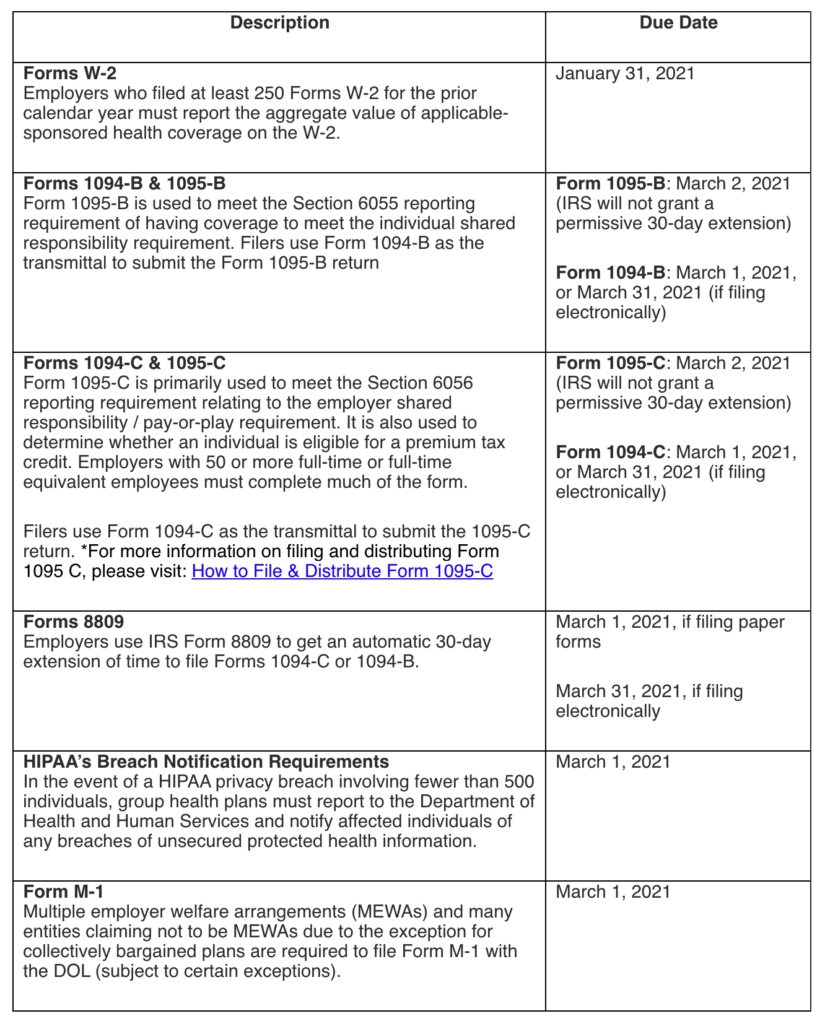

First Quarter 2021 Group Health Plan Deadlines

Medicare Part D CMS Disclosure Reminder

Each year, employers with health plans that provide prescription drug coverage to Medicare-eligible individuals must disclose to CMS whether that coverage is creditable or non-creditable. This annual disclosure must be provided within 60-days after the start of the plan year. For more information please see the attached article.

Live Well, Work Well

Health & wellness information to share with your team!

- This month’s edition features:

- 5 Ways to Start Your Year Off Right

- Kick Stress Eating to the Curb

- Don’t Forget, It’s National Blood Donor Month

- A Delicious Baked Lemon Chicken Recipe