🗓️ July 2023

Keeping HR pros up to date with important compliance, benefits, and human resources information.

Question of the Month: PCORI Fees

Q: Is there a penalty for failure to file or pay the PCORI fee?

A: Although the PCORI statute and its regulations do not include a specific penalty for failure to report or pay the PCORI fee, the plan sponsor may be subject to penalties for failure to file a tax return because the PCORI fee is an excise tax. The plan sponsor should consult with its attorney about late filing or late payment of the PCORI fee. The PCORI regulations note that the penalties related to late filing of Form 720 or late payment of the fee may be waived or abated if the plan sponsor has reasonable cause and the failure was not due to willful neglect.

All plans that provide medical coverage to employees are responsible for paying the PCORI fee. Medical coverage includes PPO plans, HMO plans, POS plans, HDHP plans, and HRAs. There are no exceptions for small employers, government, church, or not-for-profit plans. The fee must be determined and paid by the insurer for fully insured plans (although the fee likely is passed on to the plan) or the plan sponsor for self-funded plans, including HRAs. The fee is due by July 31 of the year following the calendar year in which the plan/policy year ends. Read the following FAQ for more information.

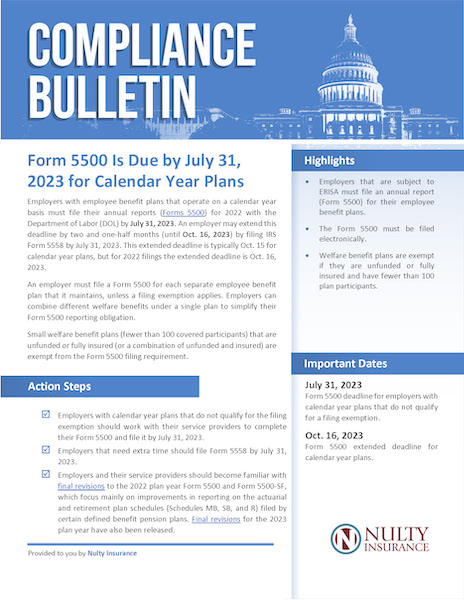

Form 5500 is Due by July 31, 2023 for Calendar Year Plans

Employers that are subject to ERISA must file an annual report (Form 5500) for their employee benefit plans. Welfare benefit plans are exempt if they are unfunded or fully insured and have fewer than 100 plan participants. An employer must file a Form 5500 for each separate employee benefit plan that it maintains, unless a filing exemption applies. Employers can combine different welfare plans under a single plan to simplify their Form 500 reporting obligation. Applicable employers must file their Forms 5500 for 2022 with the Department of Labor by July 31, 2023. Please see the following Compliance Bulletin for more information.

New CROWN Act

On June 15, 2023, Governor Whitmer signed into law the Creating a Respectful and Open World for Natural Hair Act, or CROWN Act. The CROWN Act amends the definition of “race” in the Elliott-Larsen Civil Rights Act to clarify that it includes “traits historically associated with race.” These traits include hair texture and “protective hairstyles” like braids, locks, and twists.

With the enactment of the CROWN Act, Michigan becomes the 20th state to adopt legislation that specifically prohibits discrimination on the basis of hairstyles that are commonly associated with race.

The enactment of the CROWN Act makes for great timing to review your company’s appearance standards. Please reach out to us for assistance at compliance@nulty.com.

Medical Loss Ratio Rebate

The Affordable Care Act (ACA) established medical loss ratio (MLR) rules to help control healthcare coverage costs and ensure that enrollees receive value for their premium dollars. MLR rules require health insurance issuers to spend 80-85% of premium dollars on medical and healthcare quality improvement activities, rather than administration costs.

Issuers that do not meet the applicable MLR standards must provide rebates to consumers. Rebates must be provided by Sept. 30 following the end of the MLR reporting year.

Employers that receive MLR rebates should:

- Review the rebate rules (below) and decide how they will administer the rebates.

- Any rebate amount that qualifies as a “plan asset” under ERISA must be used for the exclusive benefit of the plan’s participants and beneficiaries.

- Use this portion of the rebate within three months of its receipt to avoid ERISA’s trust requirements.

ERISA Plans

Once determined that all or a portion of an MLR rebate is a plan asset, the employer must decide how to use the rebate for the exclusive benefit of the plan’s participants and beneficiaries. DOL TR 2011-4 identifies the following methods for applying rebates:

- Rebate can be distributed to participants under a reasonable, fair, and objective allocation method.

- If distributing payments to participants is not cost-effective because the amounts are small or would cause tax consequences for the participants, the employer may utilize the rebate for other permissible plan purposes, such as applying the rebate toward future participant premium payments or benefit enhancements.

According to the DOL, using a rebate generated by one plan to benefit another plan’s participants would be a breach of fiduciary duty.

The IRS issued a set of frequently asked questions addressing the tax treatment of MLR rebates. Generally, the rebates’ tax consequences depend on whether employees paid their premiums on and after-tax or pre-tax basis.

Email us at complaince@nulty.com for more information and guidance on Non-ERISA (non-federal governmental plans) and Non-ERISA (non-governmental Church Plans).

Summary Annual Report (SAR) – Due September

ERISA requires plan administrators to give plan participants, in writing, the most important fact they need to know about their retirement and health benefit plans, including plan rules, financial information, and documents on the operation and management of the plan.

A copy of the plan’s summary annual report (SAR) must be given to participants, free of charge. The SAR is a summary of the annual financial report that most plans must file with the Department of Labor (DOL). These are filed on government forms called Form 5500. If a plan is exempt from the annual reporting requirements (Form 5500), it is also exempt from the SAR requirements.

Required Content for the SAR

DOL regulations require that certain categories of information be covered in the SAR. The SAR should include the following categories:

- Funding and Insurance Information: If a plan is uninsured, the SAR must state the types of claims the plan sponsor is committed to paying. If insured, the SAR must state the type of claims the plan has contracted with insurance carriers to pay, along with the names of the insurers and the annual premium paid

- Basic Financial Information: If plan assets are held in trust or a separately maintained fund, the SAR should include the value of the plan assets at the beginning and end of the plan year. The SAR should also include the amount of total income during the plan year and plan expenses.

- Rights to Additional Information: Individuals receiving the report have the right to request a copy of the full annual report or any part of it.

- Offer of Assistance in Non-English Language

Who Should Get an SAR?

SARs should be provided to participants covered under the plan and to those who receive a summary plan description (SPD). Electronic distribution is permissible. SARs must be given within nine months of the end of the plan year – Sept 30 for calendar year plans. If a 5500 extension was granted, the SAR is due within two months after the close of the period for which the extension was granted.

Email us at compliance@nulty.com for sample SAR language.

FORM I-9 Flexibilities Come to an End

The COVID-19 flexibilities for employment eligibility verification through Form I-9 will end on July 31, 2023, according to U. S. Immigration and Customs Enforcement (ICE). The temporary flexibilities stated that employees hired on or after April 1, 2021, who worked exclusively in a remote setting due to COVID-19-related precautions were temporarily exempt from the physical inspection requirements of Form I-9 documentation. Employers will have until Aug. 30, 2023, to complete in-person physical document inspections for employees whose documents were inspected remotely.

See I-9 Central Questions and Answers for more information.

Quick Survey

Job Market Analysis

In May, Michigan’s unemployment rate dropped to 3.7%, matching the national unemployment rate for the first time since June 2018. Furthermore, the total nonfarm payroll jobs advanced by 1.9% over the year in Michigan. See the full report

Your Nulty HR Consultants are here to help you with the ongoing labor market trends and possible challenges that go along with it. Please reach out to us for assistance at compliance@nulty.com.

New Benefit Spotlight: Long-term Care (LTC)

Long-term care (LTC) refers to a wide array of medical care, personal assistance and social support services for individuals unable to independently care for themselves for an extended period. Care can be provided in a nursing home, assisted living facility, or in one’s home.

Long-term care insurance is used to combat the high costs of long-term care by protecting individuals against incurring large out-of-pocket expenses in the future by paying affordable monthly premiums now. There are two different types of LTC insurance policies available, individual and group policies.

An LTC insurance policy covers any or all of the following types of services:

- Nursing home

- Assisted living facility

- Adult daycare center

- Home health care

- Personal care

Premiums are determined by the employee’s age at the time of enrollment. Most LTC insurance policies pay a daily maximum benefit and a lifetime maximum benefit. Most carriers offer two types of inflation protection, Automatic inflation protection and Special offer inflation protection.

Group LTC insurance may not be the right choice for all employers. Our team at Nulty is happy to discuss options and collaborate with you to see if this voluntary benefit would be valuable to your organization.

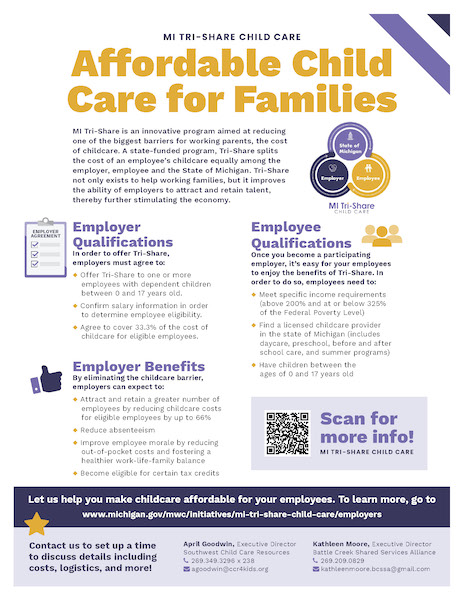

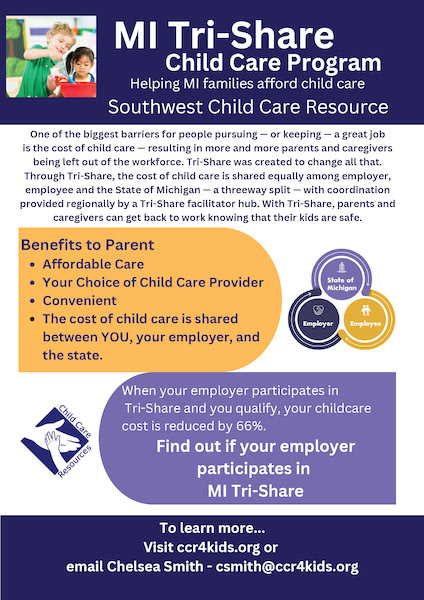

Tri-Share Spotlight

If your organization is looking for ways help employees with the cost of their childcare programs, MI Tri-Share may be right for your team!

Affordable Child Care for Families – MI Tri-Share is an innovative program aimed at reducing one of the biggest barriers for working parents, the cost of childcare. A state-funded program, Tri-Share splits the cost of an employee’s childcare equally among the employer, employee and the State of Michigan. Tri-Share not only exists to help working families, but it improves the ability of employers to attract and retain talent, thereby further stimulating the economy.